Cloud Infrastructure, AI, and the Mirage of Value

Published Oct 13, 2025

The past few years have seen an explosion in investment into cloud infrastructure and AI capabilities. Hyperscalers, chip makers, cloud providers, and AI model developers are locked in a frenetic dance of capital, acquisition, and partnership. But recent reporting suggests this dance may be more fragile than it appears — and that we may already be witnessing the contours of a bubble.

One recent article shed light on “circular financing” within the AI stack — for instance, chip companies investing in cloud or AI firms which in turn buy their chips, thereby inflating revenue and obscuring the genuine level of demand. Such deals can blur the line between real growth and financial engineering. Investopedia+2Yale Insights+2

That article argued that by acquiring one another, locking into reciprocal deals, or structuring subsidies disguised as investments, firms are propping up inflated valuations. If real end-user demand or underlying productivity gains don’t follow, that support could easily slip away.

Let’s unpack how cloud infrastructure and AI might be propelling — and possibly inflating — a bubble, and what could make it burst.

Key Deals Reshaping the AI & Cloud Infrastructure Landscape (2024–2025)

Key Strategic Deals Among Major AI & Cloud Players (2024–2025)

| 🌐 Parties Involved | 🤝 Deal / Relationship Summary | 💰 Estimated Scale | 🧭 Strategic & Market Significance |

|---|---|---|---|

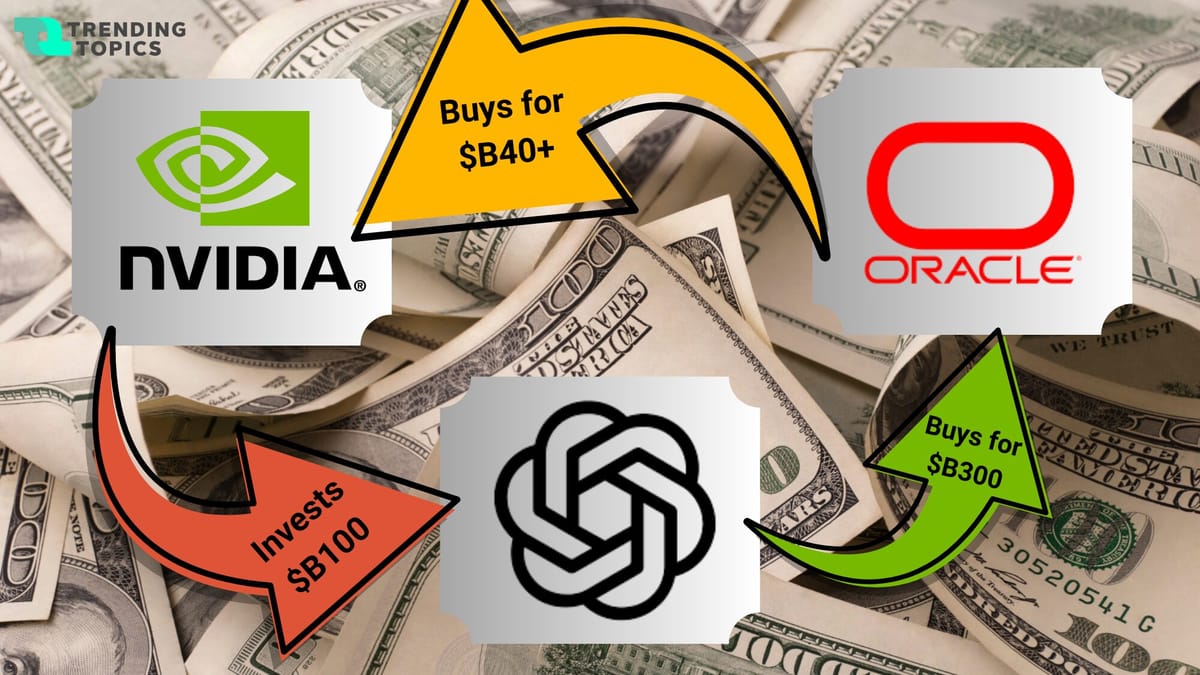

| 🟩 Nvidia ↔ OpenAI | Nvidia to invest up to $100 billion in OpenAI through GPU supply, infrastructure financing, and co-development of “gigawatt-scale” AI data centers. | $100 B+ | Anchors Nvidia as OpenAI’s primary compute provider. Creates mutual dependence — Nvidia fuels OpenAI’s capacity, OpenAI fuels Nvidia’s demand narrative. Critics note possible “circular accounting,” as investments and hardware purchases reinforce each other’s growth metrics. |

| 🔵 OpenAI ↔ Oracle | Multi-year $300 billion cloud-infrastructure contract, enabling OpenAI to run large-scale training and inference workloads on Oracle Cloud. | $300 B (multi-decade) | One of the largest infrastructure commitments in history. Deepens Oracle’s foothold in the AI cloud race. Oracle sources most of its hardware from Nvidia — forming part of an AI supply loop where investment, demand, and revenue recirculate among a small cluster of firms. |

| 🟣 Nvidia ↔ CoreWeave | Nvidia supplies GPUs and financing to CoreWeave while also buying compute capacity back from CoreWeave’s cloud. Nvidia has also taken an equity stake in the company. | $5–10 B+ | Demonstrates Nvidia’s strategy to expand indirectly via ecosystem players. While this boosts utilization metrics, analysts warn it could inflate perceived market demand through mutual revenue recognition — an echo of dot-com-era “round-trip” transactions. |

| 🔴 OpenAI ↔ AMD | OpenAI commits to deploying tens of billions in AMD’s MI300X accelerators; potential minority stake or strategic partnership discussed. | $20–30 B (est.) | Diversifies OpenAI’s hardware supply chain beyond Nvidia, providing leverage and resilience. AMD gains legitimacy as a second AI-compute powerhouse, narrowing the performance gap with Nvidia’s H-series GPUs. |

| 🟡 Microsoft ↔ OpenAI | Microsoft remains OpenAI’s largest investor ($13 billion+) and exclusive cloud host through Azure. Provides compute credits and data-center co-development. | $13–15 B+ | The backbone of OpenAI’s operational ecosystem. Microsoft integrates OpenAI’s models into Azure, Copilot, and Office, seeking long-term ROI via platform differentiation rather than short-term profit. |

| 🟠 Nvidia ↔ Oracle (Indirect) | Nvidia and Oracle collaborate to deploy Nvidia DGX Cloud and AI superclusters within Oracle data centers. | $10–15 B (infra + chip supply) | Expands Nvidia’s reach into enterprise AI workloads while solidifying Oracle as a preferred hyperscale host for Nvidia’s GPU cloud stack. This reinforces the same circular demand cycle seen in other AI mega-deals. |

Why Cloud & AI Infrastructure Are Central to the Bubble Thesis

1. Massive CapEx, Long Payback Horizons

AI — especially large-model training and inference at scale — demands enormous computing resources: GPUs, specialized accelerators, networking, cooling, power, data centers. Many companies are deploying vast infrastructure commitments before fully understanding utilization, cost structure, or demand elasticity.

In some cases, contracts are drawn out over decades, and instrumented in such a way that firms are locked into paying hefty sums. But if usage doesn’t scale, these assets could become underutilized liabilities.

2. Vendor Financing & Circular Deals

The article I referenced described deals in which a chip maker invests in a cloud provider, which then commits to buying large volumes of the maker’s chips. Such circularity can inflate perceived demand without an organic basis. Investopedia

From a financial point of view, this is dangerous: if one link in the chain falters (say, chip demand drops), the whole circular structure unravels. The illusion of robustness gives way to fragility.

3. Vertical Integration & Acquisitions

In the AI stack, there’s increasing vertical consolidation: chip manufacturers acquiring AI software firms; cloud platforms acquiring specialized modeling startups; AI firms buying infrastructure or tooling firms. A recent academic paper mapped 80 M&A deals in the AI supply chain, showing a trend toward vertical integration. arXiv

While integration can yield benefits (efficiencies, control, tighter coupling), when done too eagerly it can lead to overextension. Firms may overpay, mismanage unfamiliar domains, or misjudge synergies.

4. Valuation Premiums Unanchored to Performance

Another recent study introduced a “Capability Realization Rate (CRR)” model: it suggests a growing dislocation between AI companies’ market valuations (anchored to promised capabilities) versus the actual performance and profits being delivered. arXiv

In effect, the market may be pricing in ambitious future capabilities rather than grounded evidence. That makes the valuation highly sensitive to execution risk, regulatory changes, or evolving technology paradigms.

5. Concentration Risk & Systemic Contagion

Because a small number of large firms anchor much of the capital and infrastructure, failure or retrenchment in one node could cascade. If a major cloud provider, AI lab, or chip maker stumbles, it could trigger a domino effect across connected firms. This network effect heightens systemic risk. Yale Insights+2The Guardian+2

What the Skeptics and Supporters Are Saying

Warnings from Regulators & Institutions

- The Bank of England and IMF have recently flagged overvaluations among AI-focused firms and cautioned that the AI hype may mask vulnerabilities. The Guardian+2AP News+2

- Former tech leaders have spoken openly. Pat Gelsinger (former Intel CEO) has called the AI market a bubble, albeit one unlikely to burst immediately. Business Insider

- Prominent investors (e.g. Rajiv Jain, GQG Partners) draw direct comparisons to the dot-com bubble, warning of unsustainable “financial engineering” propelling valuations. Barron's

Counterarguments & Moderating Views

- Some Wall Street analysts argue that the “circular deal” portion of AI investment is relatively small (5–10 %) compared to the total capital flowing into AI. They contend that major tech firms have strong balance sheets and existing cash flows to absorb risk. Investopedia

- Others contend that in contrast to 2000, many of today’s tech giants are already profitable, and are funding AI investments internally—so leverage is less of an issue. Investopedia+1

- The scale of AI investment may not be purely speculative: if real productivity, automation, or new business models emerge, the foundations may hold. The question is timing and risk, rather than outright impossibility.

When & How Might the Bubble Burst?

It’s difficult (perhaps impossible) to time a bubble’s collapse, but here are plausible triggers:

- Demand Disappointment: AI applications don’t translate into sufficient revenue/fuel usage to match expectations.

- Cost Shock: Rising energy, cooling, or semiconductor costs raise the marginal cost of AI operations, squeezing margins.

- Technological Disruption: A new compute paradigm (e.g., quantum, advanced optics) emerges, making current infrastructure less relevant — akin to how fiber investments overshot demand in the 2000s. Yale Insights+2Fortune+2

- Regulation / Antitrust Intervention: Governments push back on consolidation or force divestitures, upending business models reliant on integrated control.

- Credit Tightening / Capital Dry-up: If investors lose confidence and capital becomes scarce, debt-laden or overvalued firms may collapse first, dragging peers.

When it unravels, the collapse may not be uniform. Bigger, well-capitalized players might survive; startups or leveraged infrastructure plays may be hardest hit. But ripple effects — downgrades, write-downs, loss of confidence — could destabilize adjacent sectors.

Bonus Insight: The Private Cloud Players Behind AI

While most of the attention focuses on hyperscale public clouds (like Azure, AWS, and Oracle Cloud), a parallel ecosystem of private and hybrid cloud vendors is quietly expanding to meet enterprise AI needs. These platforms enable organizations to deploy AI workloads securely, with full control over data, compliance, and latency.

| ☁️ Vendor | ⚙️ Platform / Technology | 🧠 AI Support & Capabilities | 🏭 Ideal Use Cases |

|---|---|---|---|

| Nutanix Cloud Platform (NCP) | Unified hybrid cloud solution that integrates compute, storage, and networking across on-prem and multi-cloud environments. | Offers integrated GPU virtualization, Kubernetes-based AI model deployment, and data pipeline orchestration for edge and private AI. | Enterprises running confidential AI workloads, financial institutions, and healthcare organizations with data residency requirements. |

| VMware VCF | Software-defined private cloud stack that supports vSphere with Tanzu for AI/ML workloads. | Provides AI-ready infrastructure with GPU scheduling, MLOps integration, and optimized support for frameworks like TensorFlow and PyTorch. | Suitable for regulated industries and enterprises integrating AI with existing virtualization infrastructure. |

| OpenStack | Open-source private cloud platform adopted by enterprises and service providers. | Integrates with Kubernetes, Ceph, and Horizon AI toolkits for scalable machine learning clusters. | Best suited for AI research labs, telcos, and governments seeking open-source control with no vendor lock-in. |

| Pextra Cloud Environment (PCE) | Emerging private cloud ecosystem focused on high-performance compute (HPC) and AI model training. | Supports multi-GPU orchestration, AI inference scaling, and customizable LLM hosting across hybrid topologies. | Designed for AI startups, HPC centers, and data-intensive research requiring flexible infrastructure and direct GPU access. |