Silver’s 2026 Explosion: The Infrastructure Perspective – AI Buildout, Power Grids, and the Physical Metal Crunch Fueling the Rally

Background: From the ground up: AI-driven hyperscale data centers are devouring silver for unmatched conductivity in power systems, switchgear, busbars, connectors, and thermal interfaces. COMEX vaults are draining fast—total silver at ~360.64 Moz, registered deliverable under 90 Moz (hitting ~86.1 Moz). Silver rocketed to a record $121.64/oz in January 2026 before correcting and rebounding strongly to ~$93+ by late February. Hycroft Mining (Symbol: HYMC) stands as the ultimate leveraged play on this infrastructure megatrend. Full breakdown with latest data, physical market squeeze, and charts. Especially with support from retail investors, as one of the main meme stocks.

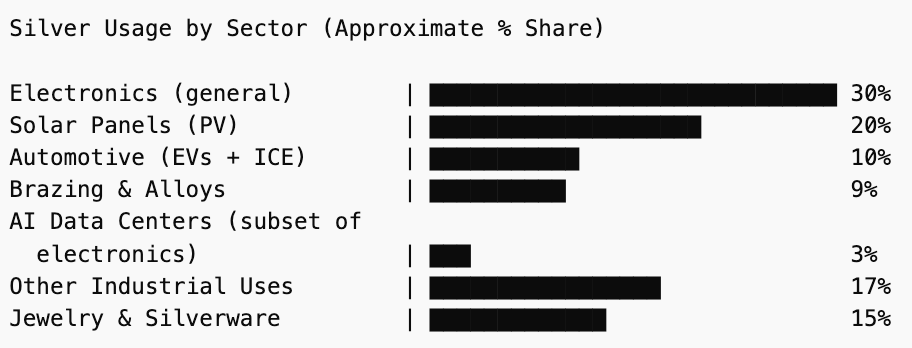

The silver market in early 2026 has transcended traditional investment narratives. It is now a raw story of physical infrastructure buckling under the explosive growth of artificial intelligence. Hyperscale data centers—the engine rooms of modern AI—demand staggering amounts of electricity, ultra-reliable high-voltage power delivery, and materials that can handle extreme thermal and electrical loads without compromise. Silver, the metal with the highest electrical conductivity (63 million siemens per meter) and thermal conductivity of any element on the periodic table, sits at the heart of this buildout: in high-current busbars, silver-plated switchgear and relays, advanced connectors for 100+ Gbps interconnects, thermal interface materials in GPUs/TPUs, and next-generation 800V HVDC architectures.

On February 27, 2026, silver futures surged more than 6% intraday, with the March contract closing in the $92.68–$93.80/oz range (settling near $92.682, up ~18.4% for the month). This rebound follows January’s explosive all-time high of $121.64/oz, a volatile mid-February correction (intraday drops as steep as 17%), and renewed buying pressure fueled by relentless physical offtake.

Silver as Critical Infrastructure Metal: The Baseline Tight Market

Silver's dual nature—monetary hedge + industrial essential—makes it volatile, but its role in modern infrastructure is what sustains the bull case. Global mine supply remains stagnant (~800–850 Moz/year, mostly byproduct), while multi-year deficits persist. The Silver Institute forecasts another deficit in 2026 (~67 Moz), even as industrial use dominates (~55–60% of demand).

Key infrastructure sectors such as solar PV, EV charging networks, 5G, and now AI data centers rely on silver's irreplaceable properties: superior conductivity reduces losses, improves efficiency, and handles high power densities without overheating or corrosion.

AI Infrastructure Boom: Power-Hungry Data Centers Driving Silver at Scale

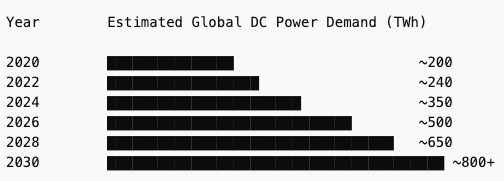

AI is not abstract code; it is extraordinarily materials-intensive physical infrastructure. Training and inference for frontier models require hyperscale facilities that can consume gigawatts—equivalent to the electricity demand of a mid-sized city. The International Energy Agency (IEA) projects global data-center electricity consumption will more than double from ~415 TWh in 2024 to around 945 TWh by 2030, with AI workloads as the dominant driver (accelerated servers growing ~30% annually).

This surge strains every layer of the electrical stack:

- Power delivery & grid interconnection: Upcoming 800V+ HVDC architectures (already being adopted in Nvidia ecosystems, with broader rollout targeted ~2027) favor silver-plated components and silver-enhanced conductors for superior efficiency, lower losses, reduced material weight, and higher reliability under sustained high loads.

- Core electrical components: Silver is essential in medium- and high-voltage switchgear, circuit breakers, relays, massive busbar systems, silver-plated high-speed connectors, and thermal management solutions inside server racks, GPUs, switches, and liquid-cooling interfaces.

- Per-unit intensity: Industry estimates show AI-optimized hardware (denser GPU clusters, advanced interconnects, enhanced thermal solutions) contains 40–60% more silver per server/rack than traditional IT equipment. A single hyperscale rack can incorporate 15–25+ grams in baseline servers, with GPUs alone using 8–12 grams in thermal interfaces and connectors. Scaled across thousands of racks per facility—and hundreds of new facilities coming online—demand becomes enormous and price-inelastic. AI rollout timelines cannot tolerate performance-compromising substitutes.

Compounding this is the renewable power buildout needed to meet data-center demand sustainably. A single 500 MW solar array (enough to help power one large hyperscale site) requires roughly 300 metric tons (~9.6 Moz) of silver in photovoltaic cells. With tech giants racing toward carbon-neutral AI, this creates powerful secondary silver pull-through.

Estimates suggest U.S. and Chinese data centers alone consumed on the order of ~350 Moz in 2025—more than 40% of annual global mine supply in some analyses—highlighting the scale of this new demand vector.

COMEX Physical Squeeze: Infrastructure Demand Is Draining the Vaults

Nowhere is the infrastructure reality more visible than in the physical silver market. COMEX inventories have collapsed amid record deliveries and industrial/institutional offtake:

- Total silver inventories: ~360.64 Moz as of February 26–27, 2026—a ~32% plunge from ~532 Moz in October 2025.

- Registered (deliverable) silver: Below the critical 90 Moz threshold, recently as low as ~86.1 Moz, with ongoing drawdowns.

- February/March activity: Among the highest delivery months on record; March open interest standing at ~52.6 Moz against razor-thin eligible stocks. Persistent backwardation and elevated open-interest-to-registered ratios signal acute spot tightness.

This is not speculative paper flows—it is real metal being pulled for deployment in data centers, grid upgrades, electrification, and renewable generation. Physical buyers (including industrials securing long-term supply) are forcing inventory out of vaults at a historic pace.

HYMC: Leveraged Play on Silver Infrastructure Upside

Hycroft Mining (NASDAQ: HYMC) owns one of the largest undeveloped silver resources in a top jurisdiction (Nevada): 562.6 Moz silver in Measured & Indicated (Feb 2026 update, +56%), with high-grade zones open for expansion.

Pre-production status means massive leverage to silver prices—once restart/PEA advances (Q1 2026 targeted), it could supply domestic infrastructure needs amid global tightness.

Eric Sprott holds ~44.5% (~36.9M shares), providing conviction and stability.

Performance: +2,000%+ over 12 months; +374% last 3 months; closed ~$50.37 on Feb 27 (after volatile swings mirroring silver).

Latest developments: Infrastructure-Driven Volatility Timeline

- Late Dec 2025 / Early Jan 2026: Surge to $121+ on AI headlines, power demand forecasts, and deficit fears.

- Mid-late Jan: Peak + initial profit-taking.

- Early Feb: Sharp correction to $70s amid thrifting concerns and overbought conditions.

- Mid-late Feb: Rebound to $93+ fueled by COMEX outflows, ongoing AI capex announcements, and infrastructure bottlenecks (e.g., grid strain reports).

Risks, Outlook & Positioning Through an Infrastructure Lens

Risks remain: potential delays in grid permitting slowing data-center builds, a broader recession crimping capex, or accelerated thrifting/substitution in price-sensitive sectors like solar. Yet the structural tailwinds—persistent multi-year deficits, AI’s price-inelastic demand, and COMEX physical reality—point to higher-for-longer silver prices.

Bull case: Silver sustains or retests $100+ (with some analysts eyeing $135–$300+ by end-2026 in extreme scenarios) as AI power demand doubles, electrification accelerates, and mine supply fails to respond through 2030 and beyond.

Investors can position via physical silver, SLV ETF, established producers, or high-beta developers like HYMC for amplified exposure to the infrastructure silver supercycle.

Conclusion – Infrastructure Is the Real Driver

Silver's 2026 run is rooted in tangible buildout: AI data centers as the new power-hungry frontier, requiring silver's conductivity edge across vast electrical infrastructure. COMEX tightness confirms the physical reality.

The bull isn't fading—it's evolving with global tech grids.

Which infrastructure angle grabs you most: AI power systems, the COMEX drain, or HYMC's potential supply role? Share below!